In the absence of inflation, interest rates have remained at record lows pushing up the value of shares and property. A turn in events is inevitable ….

The Impact of low inflation in Australia

Inflation is regularly discussed at great length in the media. Our changing economy as a result of the transition out of the mining investment boom, a depreciating yet stubbornly strong Australian Dollar, heightened competition in retailing and nominal wages growth are just some of the factors that have contributed to Australia’s current inflation rate.

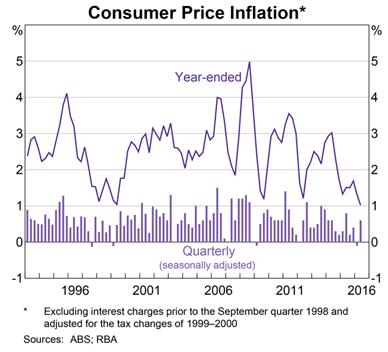

Inflation refers to the sustained increase in the general level of prices for goods and services and is measured by a CPI (Consumer Price Index). When an economy becomes inflated, it simply means that prices (in that economy) have been increasing over a period of time. Australia’s CPI for the year ending 30 June 2016 was 1.0%, materially below the 2-3% p.a. range targeted by our central bank, the Reserve Bank of Australia (RBA) and there is some conjecture around exactly what that means for the average Australian.

The concept of inflation is one that most tend to think about in terms of how it might affect their day-to-day lives: The cost of necessities such as housing, general consumer goods like groceries, fuel, transport, as well as the impact it may have on one’s savings habits. However many overlook the impact that inflation has on their investment portfolios and superannuation balances.

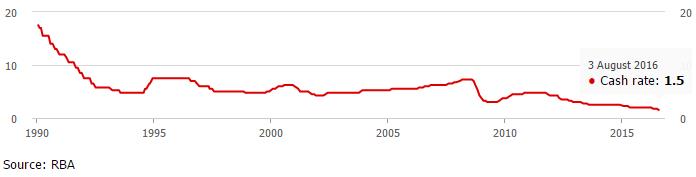

The country’s cash rate at a record low

On August 2nd the RBA announced a cut to official interest rates from 1.75% to a historic low of 1.50% in an effort to stimulate our slowing economy and avoid the slowdown that many commentators have been anxiously predicting and is now playing out in the results currently being reported by some of our largest companies such as the big banks, Wesfarmers and Telstra.

While inflationary pressures are currently lacking domestically and globally, it is important for Australian investors to avoid becoming complacent about the effects that a shift in the economic climate could have on asset prices.

A lower inflationary environment means lower interest rates and income streams

Australia, like other major economies, has experienced a sustained period of disinflation, a term generally used to describe a reduction in the inflation rate. This has led the RBA and other central banks to progressively lower the cash rate to record lows to encourage investment and stimulate the economy.

Ironically, debt markets are now pricing in the prospect of deflation (falling prices) which is far worse than inflation. As an example, investors are prepared to lend their money to the Swiss Government for 50 years knowing full well that they will get back less than they started with. Global growth is slowing and many investors are more concerned about getting their capital back rather than getting a return on their capital.

Investors seeking higher returns than those offered by bonds and cash are being forced to take on greater levels of risk to maintain income streams as returns on ‘safer assets’ such as bank term deposits continue to dwindle. Up until now (notwithstanding the associated risks) the domestic economic backdrop has been supportive for shares offering attractive and largely sustainable dividends and property (provided one has a secure tenant).

So what are central banks around the world doing to counter a deflationary environment. These statistics are worth considering:

- There has been 637 interest rate cuts globally since the start of the Global Financial Crisis.

- US$12.3 trillion in asset purchases have been made by central banks through global quantitative easing (money-printing) programs.

- There is US$15 trillion in government debt returning less than zero percent.

- There are 489 million people living in countries with official interest rates of less than zero.

Ask yourself – surely all this activity will lead to inflation at some point?

There is a commonly-held belief that investors should never try and ‘fight central banks’. In other words, if central banks want to stimulate the economy and create inflation they will succeed, and conversely if they want to slow things down and choke off inflation they can. They have unlimited firepower – no individual, company or Government can beat them.

Portfolio considerations during inflationary periods

Whilst inflationary pressures (in Australia) are lacking it is important for investors to be wary in the event of a shift in the economic climate. This is because we have experienced a sustained period of low interest rates (both domestically and globally) and investors have bid up ‘safe’ assets with ‘bond-like’ characteristics to very hefty levels in the pursuit of greater income. This could unwind quickly causing capital losses for investors (in particular those that are late to the party).

Assuming you are a believer in the ‘don’t fight the central bank’ theory, when inflation finally emerges central banks will respond by raising interest rates. Provided this is done in a slow and steady fashion (which is likely) there are some assets and asset classes that are naturally expected to perform better than others.

Shares in companies that are rapidly growing their earnings should outperform the shares of more mature businesses. Additionally, companies that can pass on higher prices to their customers can be well insulated. Companies that deliver consistent earnings will do far better than those with more volatile earnings.

Listed property trusts and direct property with leases that are linked to inflation and regular market rent reviews should hold up better than those that don’t.

Commodities like gold are often considered attractive investments due to the commonly held belief that the metal acts as a hedge against inflation because it has inherent value.

Floating rate bonds (where the interest rate payable is typically a margin over the RBA cash rate or bank bill swap rate) are considered to be more attractive than fixed rate bonds, provided that the underlying issuer is not placed under undue pressure as a result of rising costs of funding.

Not surprisingly, those that have borrowed at fixed rates can also benefit, as inflation tends to erode the liability of their debt over time. Borrowers would be wise to adjust variable rate debt to a fixed rate option, if possible.

Cash and shorter dated term deposits would also be attractive. Longer-dated bank deposits would not.

In all cases it would be wise to avoid holding investments in companies and securities with high debt levels as funding costs will rise, reducing profit margins. Reduced exposure to shares and property more broadly would be prudent as safer alternatives (such as bank deposits) become relatively more attractive.

Factors to ponder before investment markets deteriorate

No trend is permanent. Whilst it might not seem likely right now, low inflation and interest rates and rising asset prices will not last forever. With this in mind, it is extremely important to employ an investment strategy that is appropriate for your risk profile, objectives and ability to tolerate market volatility.

It would be fair to say that the longer the current environment continues the further out the risk curve investors will go to sustain their income and hence the greater the pain they will experience when interest rates and asset prices eventually normalise.

Before moving your funds out of Government guaranteed bank deposits into long dated property developments offering eye-watering returns it would be wise to give serious thought to the volatility in prices you are really prepared to accept.

Retirees will likely have far less tolerance than those younger and employed. Those with more capital can afford to ride out the cycle if a downturn emerges.

Portfolio diversification (‘not keeping all of your eggs in one basket’) is one way to minimise investment risk by spreading your wealth across a variety of different asset classes (i.e. cash, bonds, domestic and international shares, and property). Managed funds and listed investment companies that are highly diversified provide very useful roles.

Timing and identifying high quality businesses and assets are also critical factors in achieving appropriate investment returns and protecting your capital over the longer term.

Lastly, and most importantly, it would be prudent to ensure investment and superannuation portfolios are highly liquid to ensure there is the ability to reposition your assets and/or raise cash at short notice.

David Alder is a Director of Alder & Partners Private Wealth Management based in Dalkeith, Western Australia, ABN 98 146 233 534 | AFSL 382714

Disclaimer

The information contained in this release is general information only. It has not been prepared taking into account any person’s particular needs, financial situation or investment objectives, and should not be relied upon as a substitute for financial, accounting, legal, tax or other specialist advice. It is not intended to be a recommendation, offer or invitation to take up securities or other investments. You should seek advice from an appropriately qualified professional on whether the information is appropriate for your particular needs, financial situation and investment objectives.